For years, the United States fintech industry has adopted a familiar explanation for uneven adoption of new payment technologies. American consumers, the story goes, are simply slower to change than their counterparts in other regions.

A growing body of research suggests that narrative is incomplete.

Across multiple studies by payment providers, consultants, and retail analysts, a different picture is emerging. Adoption is not stalling because consumers lack interest. It is stalling because trust has not kept pace with innovation.

Trust, not novelty, determines adoption

Payments sit at the intersection of money, identity, and data. When confidence weakens in any one of those areas, behavior changes quickly.

Research from McKinsey consistently shows that consumers adopt new digital payment experiences when they believe risk is being reduced, not redistributed. Faster checkout alone rarely drives sustained adoption. Security, familiarity, and confidence do.

This helps explain why some global regions have moved faster toward centralized digital identity and biometric verification, while U.S. consumers remain cautious. Concerns about identity misuse, deepfakes, and large-scale data breaches are not abstract fears. They reflect lived experience in a market shaped by repeated, high-profile compromises of personal and financial data, as documented by The New York Times.

This isn’t just sluggishness or an overabundance of caution. In many cases, it is a rational response to a system that has asked consumers to accept more risk without seeing meaningful reductions in exposure.

Checkout is where the trust gap shows up

This trust gap is highly visible at online checkout.

According to the Baymard Institute, average cart abandonment rates remain close to 70 percent, with security concerns, forced account creation, and complicated checkout flows consistently ranking among the top reasons consumers walk away.

From a consumer perspective, checkout often requires repeated manual entry of sensitive card data across dozens of merchants. From a merchant perspective, every added layer of fraud prevention introduces friction that can suppress conversion.

This tension is not new. What has changed is scale. As digital commerce grows and fraud techniques become more advanced, the cost of weak trust frameworks rises for everyone in the ecosystem.

Why the future raises the stakes

The trust gap isn’t just a present-day problem. It constrains future progress.

The Wall Street Journal has pointed to a near future shaped by automation and agent-assisted commerce. This shift towards agentic commerce envisions AI-powered agents help consumers discover products, manage subscriptions, and complete transactions on their behalf.

That future assumes a level of confidence that has not yet been established. If consumers hesitate to trust today’s checkout experiences with their own credentials, it is difficult to imagine them delegating purchasing authority to automated systems.

Before the industry can responsibly scale automation, it must address the foundational issue of trust at checkout.

The signal from U.S. consumers is consistent

What the data shows is not resistance to digital commerce. It is selectivity.

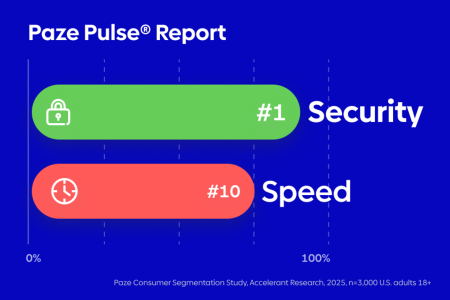

Many U.S. consumers are not asking for more features or novelty. They are looking for checkout experiences that feel familiar, that may help reduce the possibility of sensitive data exposure, and align with institutions they already trust.

This is why bank-offered approaches to checkout are receiving renewed attention. Banks already operate at scale across matters of verification and risk management. Extending that trust framework into online checkout is an evolution of existing consumer relationships, not a reinvention.

Where Paze® fits

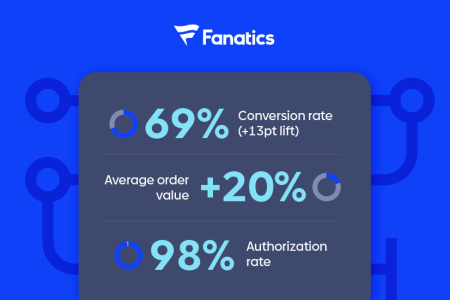

Paze® is one example of how the ecosystem is responding to this trust gap.

Offered through banks and credit unions, Paze offers added security during online checkout by hiding actual card numbers from merchants. It simplifies checkout without changing how money ultimately moves, and it anchors the experience in institutions consumers already rely on to protect their financial lives.

Rather than replacing existing payment rails or launching a standalone wallet, Paze was built as a differentiated checkout experience that favors reduced exposure and offers familiarity and confidence to consumers.

Trust scales through outcomes

Checkout trust is built through repeatable outcomes: fewer disputes, higher completion rates, better experiences at the moment of checkout.

The so-called “cautious” American consumers are not obstacles to innovation. They are a signal. When checkout becomes demonstrably safer and easier, adoption follows.

The opportunity ahead is not to persuade consumers to move faster. It is to build systems worthy of their trust.

Interested in implementing Paze or establishing a partnership? Contact the Paze team.

at checkout?

at checkout?