At NRF 2026, Paze GM Serge Elkiner and ACI Worldwide SVP Dan Coates spent 30 minutes on stage discussing the intersection of trust, payments infrastructure, and the future of commerce. Below are key excerpts from their conversation.

On Payment Diversity and Conversion

Coates: We’ve found that offering the top three preferred payment methods in a market can improve conversion by up to 30%. We surveyed more than 100 enterprise merchants — each with over $500 million in annual revenue — and saw an 11% increase in overall conversion after implementing alternative payment methods. Mobile wallets performed especially well, followed by bank transfers, buy now, pay later, cryptocurrencies, Click to Pay, and local payment methods. Does that resonate with you?

Elkiner: Yeah, 100%. About 30–40% of transactions still occur via guest checkout. That typically means the consumer either hasn’t found their preferred payment method or doesn’t trust the ones being offered. Our goal is to move consumers along a journey — from guest checkout to adopting a preferred wallet, and ultimately to a seamless checkout experience they trust.

On Why Payment Diversity Matters for Conversion

Coates: We’re seeing wallets become mission-critical — whether for billion-dollar enterprises or local fundraising organizations. Why has payment diversity become such a key driver of conversion?

Elkiner: The guest checkout numbers tell the story. In our research prior to launching Paze, roughly 50% of account holders indicated they don’t fully trust the payment methods available today. Many consumers have Apple Pay or Google Pay enabled on their devices but don’t actively use them. The missing ingredient is trust.

As a bank-offered wallet, we represent some of the largest financial institutions in the country. Consumers trust their banks. In our survey, 44–45% of respondents said they would use a bank-offered wallet if available, rather than checking out as a guest.

On How Wallets Outperform Cards

Coates: During Black Friday–Cyber Monday, we saw strong card approval rates — but wallets performed even better. Why do newer payment options improve conversion?

Elkiner: Manually entering card details is cumbersome and less secure. Consumers enter 16 digits, expiration date, and CVV — all in the clear. Wallets don't share that information. At Paze, we focus on three pillars: trust, security, and seamless interaction.

Trust: It comes from your bank. There’s no separate registration.

Security: We tokenize 100% of transactions and never share the actual card number with merchants.

Seamless: Once a wallet is claimed, checkout requires only a phone number or email and authentication via OTP or passkey.

Reducing friction increases conversion.

On Lifecycle Management

Coates: One benefit of wallets is lifecycle continuity. When a card is lost, stolen, or expired, it’s automatically reissued and reprovisioned in the wallet.

Elkiner: That’s true — but not universally. With Paze, lifecycle management is mandatory for issuers. When a card is reissued, the digital credential updates automatically in the wallet. In some other wallets, lifecycle management depends on the issuer. At Paze, it’s a rule we apply across the ecosystem.

On Conversion Benchmarks and AOV

Coates: Merchants using Click to Pay saw a 4% boost in authorization rates, checkout times 20 seconds faster, and fraud rates three times lower than manual card entry. Can you share similar benchmarks for Paze?

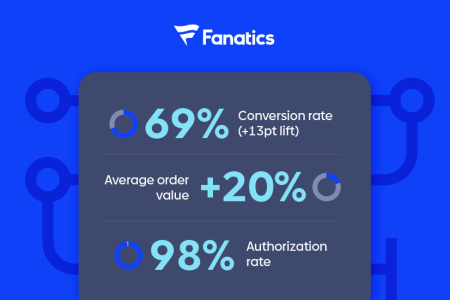

Elkiner: Fanatics integrated Paze in 2024 and saw a blended conversion rate of 69%. More notably, average order value increased by about 20% — from roughly $91 to $109. Conversion improved, and customers spent more.

We’ve seen similar patterns with Zelle®, where average transaction values tend to be higher than some competitors — likely reflecting the trust consumers place in their banks. Trust is built into the product.

On Trust and Fraud Reduction

Coates: More than 80% of consumers say they trust their bank more than any other company when it comes to payments. Additionally, 25% cite lack of trust in a site’s credit card handling as a primary reason for cart abandonment. How does trust reduce fraud?

Elkiner: Fraud reduction comes from combining tokenization with strong authentication. When issuers see that a credential was provisioned and authenticated within Paze, confidence increases. That linkage — between the pre-provisioned financial credential and verified end-user authentication — supports higher approval rates with lower fraud risk.

On How Trust Changes the Payments Landscape

Coates: As payment types proliferate, how will trust shape the future?

Elkiner: Consider agentic commerce — where AI agents transact on your behalf. Which agent do you trust with your payment credentials? Thousands of independent agents? Big tech platforms? Or your bank or credit union?

A trusted wallet can provide transaction-specific tokens to agents, limiting exposure. Even in physical retail, transactions increasingly begin digitally — ordering ahead with mobile orders at Starbucks or Dunkin’, for example. Commerce is becoming omni-channel by default. That requires a secure, trusted credential environment.

On Real-Time Payments and the Wallet as a Container

Coates: Under Early Warning Services, do you see real-time payments being incorporated into Paze in the future?

Elkiner: Paze is a wallet and a container. Over time, it could support multiple payment methods — not just credit and debit cards. Since debit cards connect to bank accounts, additional rails could potentially be integrated. The priority is understanding which methods consumers value most and ensuring proper authentication and security.

On Stablecoins

Coates: Stablecoins have sort of won the race with the Genius Act passing. Could you potentially foresee crypto being available through the Paze wallet?

Elkiner: Stablecoins have certainly been one of the most discussed topics recently. Early Warning Services announced plans to pilot stablecoin functionality through Zelle® International for cross-border transactions.

We’re evaluating use cases carefully. Beyond crypto trading, holding U.S. currency in high-inflation markets, or cross-border payments, the applications are still emerging. We’ve decided to test and learn.

On The Future of Wallets

Coates: What does the future hold for Paze and the industry overall?

Elkiner: The future hinges on trust and security. Authentication and digital identity will become as important as the payment credential itself. The real opportunity lies in marrying identity with financial credentials.

Markets like the Nordics demonstrate this model with BankID integrated into wallets — delivering high approval rates, low fraud, strong conversion, and deep consumer trust.

Final Thoughts

Coates: Anything else you’d like to leave the audience with?

Elkiner: It’s an exciting time in payments. Merchants are focused on improving conversion, while payment methods continue to proliferate globally. There’s no single universal method — in Brazil, you need Pix; in Argentina, Mercado Pago. Success increasingly depends on combining payment diversity with trust and security. I think it's a fascinating time to be in payments and for myself to work with some of the largest merchants in the world. It's important for those merchants to have their payment stack be agile and future ready.

Interested in implementing Paze or establishing a partnership? Contact the Paze team.

This transcript has been edited for clarity and length. Remarks reflect a live conversation between Serge Elkiner, GM of Paze, and Dan Coates, SVP at ACI Worldwide, at the National Retail Federation Big Show, January 2026.

at checkout?

at checkout?